OTS may not deserve some criticism from its performance during the financial crisis.

One question posed by the recent financial crisis was whether our confusing and disaggregated approach to financial regulation in the United States was to blame for the downturn. Did our regulators fail to identify weaknesses in the financial intermediaries they oversaw that they should have seen?

Dain Donelson and I attempted to answer part of this question by studying the performance of the Office of Thrift Supervision (OTS) during the crisis. OTS was the smallest federal banking regulator, the one most criticized by Congress for its performance, and the only agency sanctioned in the Dodd-Frank Act: it was eliminated, and its functions were moved elsewhere in the Treasury Department. Our research examined a particularly disparaging criticism of OTS: did this agency offer banks soft touch regulation as a way of competing for supervision fees against more rigorous regulators?

We did not find much evidence in support of this oft-proffered view. We compared thrifts to banks, charter-switchers, which are institutions that took up or gave up thrift charters in the years leading to the crisis, to other thrifts and banks, and bailout recipients to non-bailout recipients to discover if any of these institutions did poorly when compared to their peers during the financial crisis.

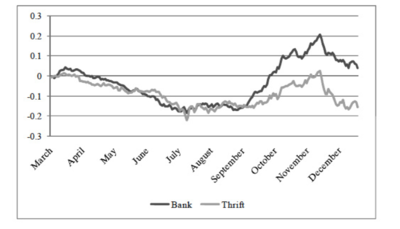

In our comparison of publicly traded thrifts with publicly traded banks during 2008—the critical year of the crisis—we found that thrifts fared only marginally worse than banks, if at all, during that year. This result modestly suggests that the multi-regulator regime, however illogical, did not concentrate instability in a particular industry subject to a weak regulator.

Likewise, when we compared thrift and bank performance to those institutions that chose to switch regulators immediately before and during the financial crisis, we found no significant differences in returns among either institutions that converted their federal bank charters to federal thrift charters, or institutions that their converted federal thrift charters to bank charters, although our samples of these institutions are small.

Finally, in examining the bailout propensity of these charter-switchers, our results suggested that institutions switching to thrift charters were big enough to receive bailout money from the government, but they did not. Conversely, we found that institutions switching away from thrift charters received more bailout money than their size would suggest. This finding may suggest some, possibly misplaced, dissatisfaction with the performance of OTS among federal government officials, which may have contributed to the decision to eliminate it in the Dodd-Frank Act passed in the wake of the crisis.

returns for publicly banks and thrifts during 2008 tracked each other quite closely. And, when thrifts started doing worse than banks, towards the end of the year, the difference was not statistically significant. The accompanying table shows the cumulative adjusted returns for thrifts and banks during 2008.

returns for publicly banks and thrifts during 2008 tracked each other quite closely. And, when thrifts started doing worse than banks, towards the end of the year, the difference was not statistically significant. The accompanying table shows the cumulative adjusted returns for thrifts and banks during 2008.